When Techbros’ Circle Jerk Becomes a Circular Firing Squad

[NB: check the byline, thanks. /~Rayne]

I have been meaning to write a longer post about this topic but the events of the last 48 hours have forced me to stop snickering long enough to put up this post.

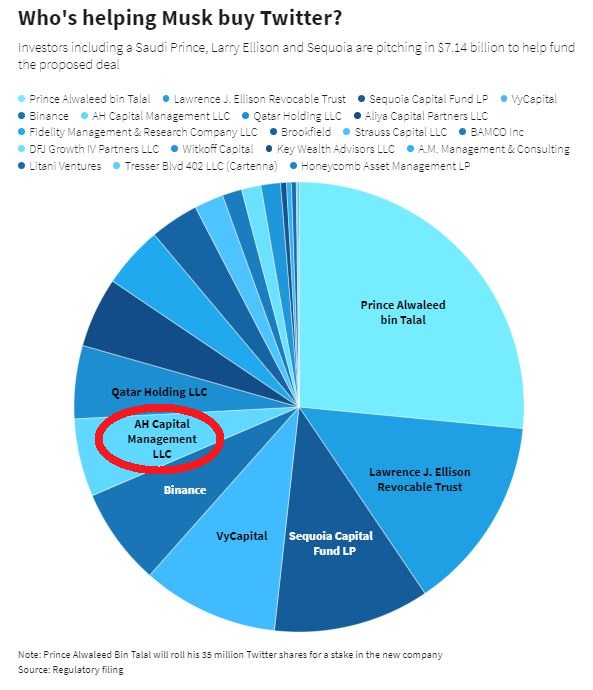

Here is a chart depicting Twitter’s current investors comparing their relative amount of commitment:

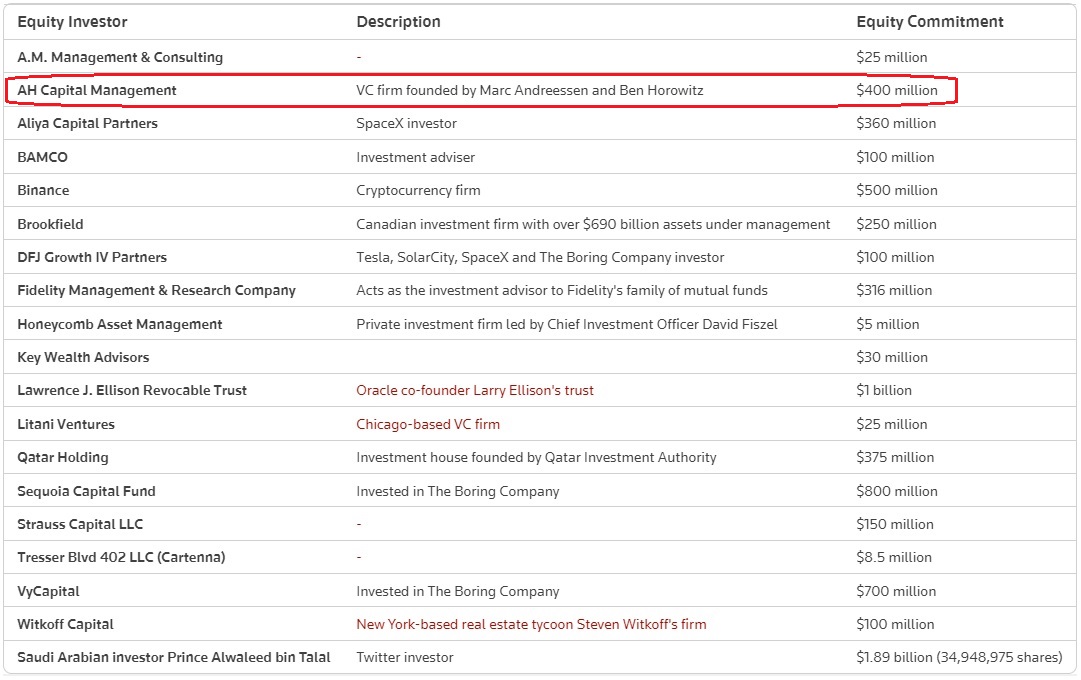

Here is a list of the investors’ names and the amount they’d committed at the time Elon Musk closed the deal to acquire Twitter.

In both graphics from Reuters above I’ve noted in red one name in particular — that of AH Capital Management, LLC.

A as in Andreesen, H as in Horowitz. As in the venture capital firm behind a16z.com.

As in the venture capital firm behind Substack.

Elmo is pissing on one of his investors because his investor’s investment decided to launch a competing platform.

Let that sink in, as Elmo so eloquently tweeted as he dragged a bathroom fixture into Twitter’s offices last October.

~ ~ ~

Axios beat me to making the observation about the financial relationship between Elmo’s Twitter and AH Capital in their article yesterday about Substack’s recent fundraising effort relying on crowdfunding.

Substack announced the offer to sell equity to writers on March 28, with its own writers’ investments prioritized over others who might choose to participate.

The fundraising effort followed an aborted fundraising attempt last year.

As Axios’ Dan Primack noted, the crowdfunding prospectus didn’t report this year’s financials, only the previous two years as required by law.

Substack’s founder Chris Best apparently believes Substack “doesn’t actually need the money,” forecasting profitability ahead.

This makes little sense to me.

What does make sense, though, is that the VC funding well may have run dry.

Take a look at the Form ADV – Uniform Application for Investment Adviser Registration and Report by Exempt Reporting Advisers, filed on March 31 this year with the Securities and Exchange Commission by AH Capital Management (hereafter a16z).

Caveat: it’s more than 400 pages long, might take a bit to browse.

I regret not downloading a copy when I first read this document in mid-March. I’d lost count as I scrolled through the form back then while counting the number of times SILICON VALLEY BANK and SVB appeared in the document as a second custodian for private funds.

You’ll recall SVB collapsed on March 10 this year.

The version of a16z’s Form ADV now shows SILICON VALLEY BANK, A DIVISION OF FIRST CITIZENS BANK reflecting the post-crash acquisition of SVB as part of a rescue plan. This new identity appears 84 times, with other financial management firms like J.P. Morgan, Merrill Lynch, and Raymond James each appearing in tandem but fewer times as fund custodians. None of the others appear as frequently as SVB.

While these financial managers are custodians, the frequency with which SVB is mentioned in a16z’s filing suggests a repeated relationship with SVB apart from fund custodian.

Is Substack’s renewed fundraising effort due to tightening of a16z’s financing capacity, possibly due to losses at SVB?

The Substack financials provided to potential crowdfunding investors certainly won’t shed light on their funders’ conditions.

~ ~ ~

What’s much more obvious about Substack’s recent launch of a microblogging platform “Notes” to complement its blog/newsletter format is its potential to draw down users from Twitter.

Substack Notes must also have cost some cash to develop and now going forward to administer.

It’s not clear whether the new microblogging platform will eventually offer an alternative source of monetization. It’s possible that Substack longform could remain subscription based as one revenue stream while Substack shortform could sell promoted Notes or advertisement space (Tumblr users will understand the advertising possibilities using scroll over content).

With advertisers abandoning Twitter causing its advertising revenue to tank by 89%, there’s money on the table out there somewhere waiting to be chased by a microblogging platform which isn’t a crustpunk Nazi bar. Is Substack positioning itself to sweep up some of the cash?

They may need to if Substack can’t go back to the VC well. Offering equity may be a way to ensure their longform writers stay on board with a change in business model since they may be happy to increase their earnings without having to hump more subscriptions.

There’s a limit to the subscription market, after all. How many subscriptions can the average reader afford?

~ ~ ~

It’s not just the possibility that the VC well has been affected by SVB’s crash; it’s the rolling damage to funding capacity caused by cryptocurrency ventures.

You’ll note in the Twitter financing graphics that cryptocurrency exchange Binance is a financier to Musk’s Twitter. Binance has been under investigation by the Internal Revenue Service and the Department of Justice; the latter has been split over whether to file criminal charges against Binance.

Fallout from the collapse of cryptocurrency exchange and hedge fund FTX also figures into the mix; it’s difficult for the public to readily determine which investment managers were exposed and how deeply unless the investment manager was so deeply over their heads in FTX that they are obviously failing — like Silvergate Bank which folded on March 9.

At that point it becomes an ourobouros eating itself since Silvergate’s collapse preceded and helped precipitate SVB’s collapse.

How much of Elmo’s desperate and sloppy flailing after cash through half-assed approaches like his new Twitter Blue is tied to the inability to seek more financing through non-traditional sources?

~ ~ ~

The stupidest part of all of this is that techbros did this to themselves through their own stupid hubris. Stupid, in that they didn’t bother to do their homework early enough to prevent this financial Jenga.

Hubris, in that they’ve acted like the rules don’t apply to them, as if they’ve got enough money they can throw it around endlessly without any concern they may be held accountable, as if rubbing their shoulders with people like themselves in their own circle is all they really need to assure their ongoing success.

Peter Thiel decided it was all about him and his immediate best buddies related to the Founders fund when he set off the bank run at SVB.

Never mind how this might affect the rest of the tech sector ecosystem, or the other non-technology businesses which had been persuaded to use SVB for their banking needs.

The PayPal Mafia-spawned techbro-hood finally failed its acolytes and the damage has yet to be fully realized.

“I had $50m of my own money stuck in SVB,” Thiel told the Financial Times, omitting what you might imagine as the natural follow-on, “I can’t help it if I could run faster than the rest of you ahead of that grizzly bear gaining on us after I tweaked its nose.” But $50 million is loose change stuck in the cushions to a guy who made a billion on cryptocurrency, fortunately before the crypto-tulip mania began to crater.

Marc Andreesen and Ben Horowitz at a16z should have noticed much earlier that far too many of their investments overlapped either in the other financing on — like cryptocurrency exchanges — which they relied, or in the personalities of the techbros’ involved.

Did they buy into the hype about Elmo like so many Muskian fanbois? They could have done the legwork and discovered for themselves quite inexpensively what it is that Elmo didn’t want revealed in DE’s Chancery Court so badly that he scrambled out of exposure and simply closed on Twitter.

And then the others who have relied on a16z for funding like Chris Best at Substack, and all the writers who’ve signed up with Substack, all now hanging on to whatever it was that sold a16z about Elmo’s Twitter and the techbro ecosphere which banked at SVB…

Including Noam Bardin and Post.Media (Post Media, Inc.) which also received funding from a16z to launch as a Twitter competitor. The platform has not taken off as anticipated, its Terms of Service seen as stultifying and its flat excessively polished effect discouraging to building out social networking.

~ ~ ~

One other thing all these techbros who are pulling rugs out from under each other have in common: their age. The oldest are in their mid-50s and the youngest in their mid-40s. They’re old enough to have adult children, old enough not to want to sleep on the floor in their offices amidst pizza boxes and empty soda cans. Perhaps all of this bullshit circular firing squad among the techbros which leave us as collateral damage is really just a nasty mid-life crisis.

We should worry when they finally begin to clue into their mortality — one of them has already been eyeing the blood of teenagers for infusions as a fountain of youth, out of some sort of sick techbro vampirism. As if our social media environment and our nation’s economic welfare aren’t enough blood to siphon off.

The entire technology environment from social media to apps to network to cloud is ripe for a generational shift, a generation which won’t see the current techbros as the end-all-be-all of financing and development.

A generation used to being told to suck it up by guys who were born into wealth, hung out with wealthy tech dudes, and blinded by their own wealth, a generation used to screaming for relief while billionaire techbros blithely look to their own backsides is coming of age.