Empirical Test of Piketty’s r > g Theory Coming

Bernie Sanders forced the issue of wealth inequality into the presidential campaign, which presented a real problem for neoliberals of the Democratic persuasion. They want us to believe that the market rewards people in accordance with their merit and hard work. It doesn’t. They want us to believe everyone can get ahead if they get a good education and work hard. Not so. So the neoliberal dems fall back on their version of trickle-down: economic growth is the cure. So what is the future of economic growth?

Earlier this year Gerald Friedman did a study of the potential impact of Bernie Sanders’ economic ideas, saying they would create enormous economic growth. That drew fire from many liberal economists, including Paul Krugman who wrote several blog posts saying Friedman’s numbers were ridiculous, and using that as a opportunity to bash Sanders supporters for naiveté and for encouraging impossible expectation. On February 23, he put up a post with his own predictions of growth: a fraction over 2%. And that, he says, is good enough.

And let me say that the great thing about a progressive agenda is that it doesn’t require big growth promises to make it work, because the elements of that agenda are good things in their own right. Conservatives need to promise miracles to justify policies whose direct effect is to comfort the comfortable (cutting taxes on the rich) and afflict the afflicted (slashing social insurance); progressives only need to defend themselves against the charge that doing good will somehow kill economic growth. It won’t, and that should be enough.

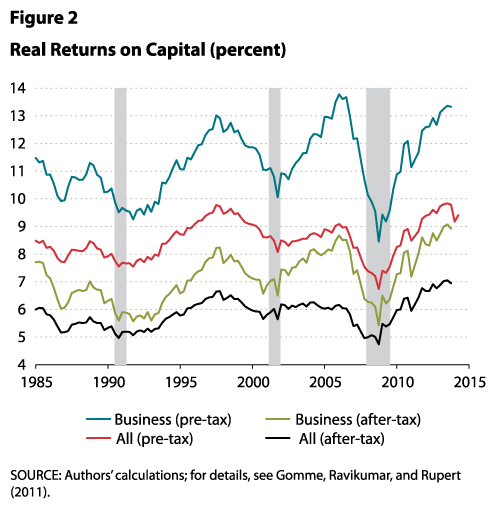

But what about inequality in this scenario? Thanks to Thomas Piketty and his book Capital in The Twenty-First Century, we can say with some certainty that it isn’t going to get better with this kind of thinking. Remember Piketty’s basic finding: if r > g, wealth inequality will increase to a very high level. In this formulation, r is the rate of return to capital, and g is the growth rate of the economy. Here’s a chart from the St. Louis Fed showing the rate of return to capital in the US:

With the exception of the immediate post-Great Crash years, the All capital after tax line doesn’t sink below 5%, and the most recent figures show it near 7%. Here’s the definition, found in Note 5:

“Business” capital includes nonresidential fixed capital (structures, equipment, and intellectual property) and inventories. “All” capital includes business capital and residential capital.”

Piketty’s definition of capital is broader than this definition of “all”, but there isn’t any reason to think that will have a material effect on the overall number. In other words, r is about 5% higher than g, so we can expect a steady increase in wealth inequality.

The Republicans couldn’t care less: they nominated a billionaire. What’s on offer from the Democratic Party? Here’s Hillary Clinton’s webpage on economic issues. It’s mostly neoliberal ideas, from cutting taxes to deregulation to trade (see the part on small businesses), and some liberal ideas: investment in infrastructure and research, equal pay, paid leave and affordable child care. Her new idea? Let’s give tax breaks to companies that share profits with workers. Also, raise the minimum wage to $12 some day, and some tiny steps to increasing taxes on the rich by closing loopholes and making sure rich people pay more taxes than Warren Buffett’s secretary.

We are going to get an empirical test of Piketty’s idea, but we already know how it will turn out. The rich have nothing to fear.