Days before an October 7, 2022 meeting at which, Gary Shapley has claimed for months, his “red line” was crossed, the thing he has used to excuse months of leaking as “whistleblowing,” he scripted the things — including a demand for a Special Counsel to make the decision that David Weiss announced having made in the meeting — that Shapley claimed to record in real time at the meeting.

Indeed, the documents House Ways and Means released last month purporting to support their complaints about the Hunter Biden prosecution show that Shapley’s tantrum had been going on for weeks and had started in significant part because the charges he was demanding wouldn’t be rolled out in advance of the 2022 election.

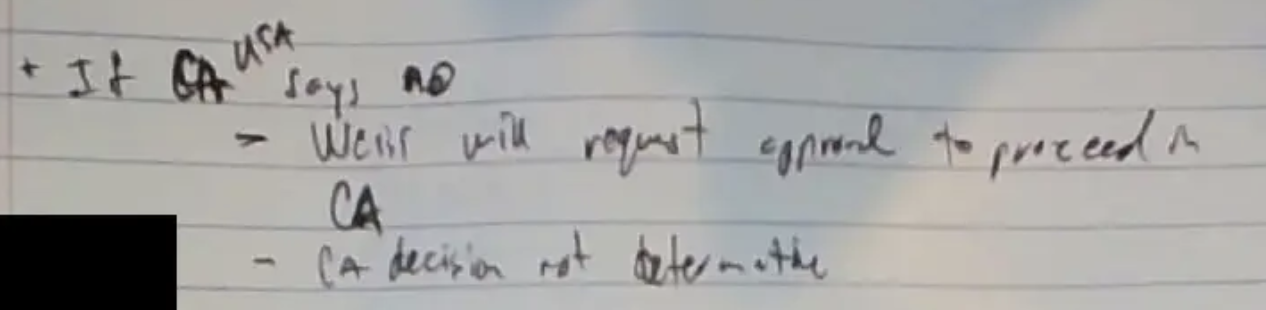

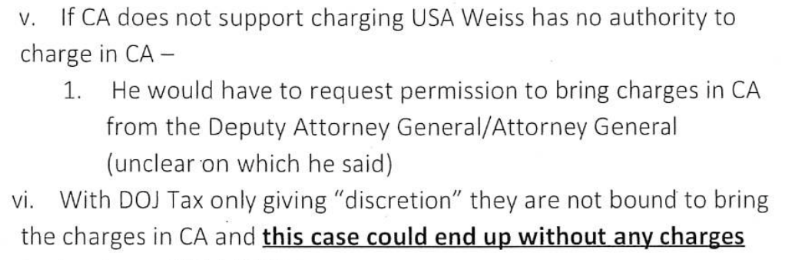

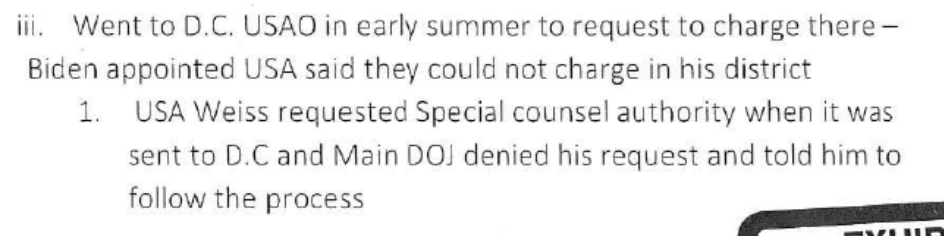

It has already been established that no other attendee at the October 7, 2022 meeting has backed Gary Shapley’s version of that meeting. No other attendee remembered David Weiss conveying that he didn’t have the authority to make this charging decision regarding Hunter Biden on his own. Most attendees have charitably explained that Shapley didn’t understand what he was hearing, particularly with regards to Special Attorney versus Special Counsel status. In his testimony to the House Judiciary Committee, Matthew Graves attributed Shapley’s claims to, “the garble that can happen when you layer hearsay on top of hearsay on top of hearsay. And when you look at a lot of this, it’s someone said that someone said that someone said.”

Even just Shapley’s own notes undermine his claim. As I have noted, between his hand-written contemporaneous notes and his emailed memorialization, Shapley reordered how things happened at the meeting, moving the reasons Weiss gave on October 7 for why he wouldn’t charge 2014 and 2015 — the charges against Hunter Biden that would have to be charged in DC — after Shapley’s own claim that David Weiss didn’t have the authority to make that prosecutorial decision.

Per his contemporaneous notes, the first thing discussed after the discussion about the leak was Weiss’ rationale for not charging 2014 and 2015, the two more substantive years that would have to be charged in DC. Once you’ve explained that, then whether or not Weiss got Special Attorney status for DC is significantly moot (2016 was only ever treated as a misdemeanor).

In his email to his boss, though, Shapley moved that discussion to after his argument, covering the DC charges, the LA charges, and the involvement of DOJ Tax Attorney, that Weiss didn’t have authority to charge. If Weiss had already explained his prosecutorial decision about the most problematic Burisma years — something Shapley’s hand-written notes record him has having done — then none of the other complaints about these years (that Weiss or Lesley Wolf let the Statutes of Limitation expire, that Weiss didn’t get Special Attorney authority in DC) matter. Shapely reorders his notes to hide the fact that the DC decision didn’t matter.

Shapley’s hand-written notes record Weiss sharing a prosecutorial decision — not to charge the 2014 and 2015 tax years. By making a decision not to charge in DC, Weiss was exercising the prosecutorial authority Shapley claimed Weiss said he didn’t have. Once you describe Weiss making a prosecutorial decision, then any claim that he didn’t have prosecutorial authority crumbles.

It crumbles even more given a few other details.

Shapley’s retroactive memorialization of the October 7, 2022 expresses great fury over Weiss’ decision not to charge the 2014 and 2015 years, as well as the delay of charges until after the election.

But Shapley learned of this weeks and even months earlier.

On July 29, for example, Joseph Ziegler asked Lesley Wolf about timing. Per Shapley’s own memorialization, she said Weiss was aiming to indict before the end of September, but Wolf herself expressed doubt that would happen. That comment on timing, coupled with her stated disinclination to toll the 2014 tax year, was a pretty solid indication that she was disinclined to charge 2014.

Zeigler

Any dates or goals?

Wolf

David has indicated that the end of September would be his goal to charge. The is reflective of keeping everything on track. They do not want to get any closer to a mid-term. If doesn’t happen by end of September it would have to wait until November after the elections. She stated she does not think that is likely to by charged by September.

Sol on 2014 blows on November 8, 2022.

X Factor on timing will include any delay defense counsel has requested and that they would be amenable to toll statutes. She is not leaning toward tolling again…but it is possible.

Current plan is that the prosecution recommendation will be collaborative with DOJ Tax and USAO.

[snip]

They will communicate any decisions on specific tax years and decision to charge or not charge to the prosecution team in advance of any final document. [my emphasis]

On August 16, the IRS investigators had a meeting with David Weiss, one that Wolf happily arranged on August 8. Because Wolf and other DOJ personnel could’t attend, that would be a second meeting the IRS had with David Weiss alone.

On August 11, DOJ Tax tried to set up a meeting for the following day, an invitation which Ziegler accepted; Shapley was not invited. There’s no memorialization of this meeting, at which DOJ Tax probably explained why it viewed the 2014/2015 tax years as weaker charges.

On August 15, in advance of the meeting with Weiss, Shapley reminded Darrell Waldon and Michael Batdorf about the forthcoming meeting with Weiss. Only Michael Batdorf, the second-level supervisor who testified that Shapley had a habit of, “a tendency to go to level like grade 7 five-alarm fire on everything,” responded. Shapley’s August 17 memorialization of the August 16 meeting, shared with those supervisors again, showed that Weiss was “leaning” towards only charging the CA charges, 2017 to 2019. Shapley recorded Weiss aiming to charge by the end of September, but said himself it’d be “October/November” (even though, in July, Wolf had said that if it wasn’t charged by September, it would be after November).

Here’s what Shapley said about 2014 and 2015 in that email:

We again pushed back on not charging 2014/2015. DOJ Tax continues the position that the defenses (load/taxes paid by another person on half the income) would make it too complex for the jury. I believe their position is unsupportable–both considering precedent and evidence. I made it clear that not only do we disagree with that position but that we could provide countless prosecution recommendations that included diverted income to nominees and various loan claims to support our position. The USA agrees with us but then talks to DOJ Tax and they convince him otherwise. This has happened a couple times. As a result, we will continue to communicate our position to ensure this moves forward consistent with how other tax cases would be treated with similar fact patterns.

I explained that 2014 is not charged how it would severely diminish of the overall conduct and would essentially sanitize some major issues to include the Burisma/Ukraine unreported income. I also explained that if 2014 is not charged and/or included in a statement of facts in a guilty plea, that the unreported income from Burisma that year would go untaxed. I believe leaving out 2014/2015 would deliver a message that is contrary to IRS’s efforts to promote voluntary compliance. [my emphasis]

Some of this is about getting taxes paid — the explanation Shapley would repeat in his memorialization of the October 7 meeting. But some of it is about tying Hunter’s tax crimes to Burisma.

Once again, Batdorf was the only who responded. He said he would escalate Shapley’s concerns still further, so the Chief and Deputy Chief of IRS could “at least show full support for the 2014/2015 years.” In Waldon’s testimony, he expressed being surprised at the October 7 meeting, because “I was not fully aware of a decision regarding some of the investigative years,” (49) a view that may stem from Shapley’s efforts in August to reverse this decision.

On August 18, Mark Daly from DOJ tax sent the investigative team (but not Shapley) an email that seems consistent with presenting to grand juries in both Delaware and Los Angeles in September — but not DC, once again consistent with a decision not to charge 2014 and 2015. Of note: this email was saved on June 27 of this year, before Ziegler and Shapley testified to the Oversight Committee on July 19 and Ziegler offered to go back to find more materials. Ziegler appears to have already taken steps to share information that he feigned was just a response to Congressional inquiries.

Shapley appears to have memorialized an August 25 email from Lesley Wolf asking a newly added FBI agent, along with Ziegler and Mark Daly, not to use email to coordinate between meetings. Shapley wasn’t a recipient of this particular email. It’s an example of the double set of books Shapley confessed to in his original deposition.

On September 20, 2022, over a week before the interview of James Biden (Hunter’s uncle and sometime business partner and Joe’s brother) and the day after Martin Estrada was confirmed as US Attorney for Los Angeles, Shapley emailed Weiss, cc’ing no one else, asking for a call in the following two days. The next day, September 21 at 1:23PM, Weiss said he would set up a meeting “in the near term,” including IRS and FBI, to provide an update. This email thread, which Shapley would pick up over a month later, would become the one where Shapley’s paranoia about Weiss cutting off communication with Shapley first expressed. As we’ll see, this Shapley request to Weiss was also the ultimate genesis of the October 7 meeting.

Just over two hours after Weiss promised an update shortly on September 21, Shawn Weede, Weiss’ Criminal Chief, wrote to set up the meeting Weiss had promised, proposing the meeting for September 28 (still one day before the interview of James Biden). Shapley responded 22 minutes later, noting that he would be in the Netherlands on the day of the proposed meeting, but would be willing to call in.

The next day, at 11:15AM, Weede wrote back to say a “sanitized” meeting was unworkable, and so proposed the meeting for the week of October 3, after Shapley got back.

Also on September 22, Shapley memorialized a meeting that started at 2:30PM noting that Lesley Wolf and DOJ Tax’s Mark Daly joined the meeting late, but without documenting anyone else who attended. The memorialization was closely focused on briefings of Estrada’s office on the case (though Shapley refers to Estrada as “her”). It also clearly records DOJ tax still conducting their review, as well as a decision not to charge either the gun charge and/or anything else until after the election — precisely the eventuality that Wolf had warned would happen almost two months earlier.

Gun charge will likely not be indicted in October.

[snip]

USAO and DOJ Tax made the decision not to charge until after the election. They said why should they shoot themselves in the foot by charging before.

Within an hour after the start of the call, Shapley was going ballistic about precisely that eventuality. Starting at 3:34PM, Shapley alerted Batdorf — but not his immediate supervisor, Waldon,

Big news on Sportsman. Joe Ziegler and I need to speak with you as soon as possible.

In a follow-up, Shapley explained that the “bad news” he had was precisely what he had been warned about in July, that the charges would be delayed until after the election.

Bad news. Continued inappropriate decisions affecting timing. i.e. Election. We can talk later if you are busy….I believe their actions are simply wrong and this is a huge risk to us right now.

Note: There was no risk to the IRS of delay after the election. It would mean the 2014 charges would toll (unless Hunter’s lawyers agreed to waive tolling, as they had before), but that’s another thing Shapley was warned about. A significant part of Shapley’s tantrum seems to stem from a personalized concern that charges would not come out before the election.

Batdorf ended the exchange by instructing, “Please ensure your ASAC and SAC are updated as well.”

Shapley did that, but not until almost two hours later, in a 5:28PM email to Darrell Waldon (his ASAC), Lola Watson (his SAC), and Michael Batdorf. Without noting that he had already bypassed chain of command, Shapley complained,

During todays SM call there was some information provided to the team concerning decisions made by the USAO and DOJ that need to be discussed. For example, the AUSA stated that they made a decision not to charge until after the election. In itself, the statement is inappropriate let alone the actual action of delaying as a result of the election. There are other items that should also be discussed that are equally inappropriate.

None of those other items “that should be discussed” were obviously reflected in his memorialization of that call.

At least on paper, this tantrum, made two weeks before a pre-election leak to the WaPo, was about something he had been warned of in July, not news at all, but one tied — explicitly in his mind — to the election, not timing per se.

Side note: Unlike Ziegler’s, many of the documents Shapley shared are stripped of all metadata. Not this email, though. This email — which he shared twice (Attachment 5, Attachment 24) — both reflect a creation date of September 20 (this is European notation), over eight hours apart, with the second reflecting Tristan Leavitt as document author.

That would mean these documents were saved after Darrell Waldon (September 8) and Michael Batdorf (September 12) testified. There’s good reason to believe these documents were chosen with some knowledge of the IRS supervisors’ testimony.

To make it plain: For months, Gary Shapley claimed that his red line was crossed on October 7, 2022. But the emails he himself turned over show that’s not true. His red line was crossed on September 22, 2022, and the red line had a lot to do with making charges public in advance of the election.

Importantly, that means his red line was crossed before the leak to the WaPo, not afterwards.

The day after Shapley’s tantrum started — which no one at DE USAO or FBI would have known about — the FBI ASAC seconded the plan to wait until Shapley returned before holding the meeting that would become the October 7 one, noting that then Weiss could be present.

Meanwhile, on September 28, Waldon emailed Ziegler and all the other people Shapley had involved in his tantrum, noting that he was trying to arrange a meeting with Weiss and Poole. Ziegler responded to everyone, on the morning of September 29, promising any update from prosecutors in CA. Waldon responded asking Ziegler to call him. And Ziegler responded, suggesting they should do a pitch on the 2014 and 2015 years to DC prosecutors: “we also need to request the presentation of 2014 and 2015 to the criminal chief / US attorney in DC – similar to what we would do in California for 2017 2018 and 2019.” Again: Waldon seems to have been surprised when, at the October 7 meeting, Weiss announced that the decision had been made.

That was at 11:11AM on September 29. At 2:25PM, Ziegler went into the interview with James Biden, Hunter’s uncle. Lesley Wolf and two other prosecutors who, like Ziegler, would not be at the October 7 meeting, also participated in the interview. The interview focused largely on the 2017 to 2019 years (though also asked questions that might reflect a campaign finance investigation into Kevin Morris), but which Ziegler now points to as critical testimony supporting his argument for felony charges in 2018. Shapley was already a week into a tantrum about charges not being filed before the election before this interview.

Seven minutes after the James Biden interviewed finished — based on public records, at least, the last major investigative step in the investigation, Weede proposed and the ASAC confirmed a meeting for October 7 at 11AM. The FBI ASAC confirmed as well. Then the next day, a Friday, the ASAC followed up to confirm once again, management and investigators would be present. She followed up again at end of day Monday, October 3, confirming she and her boss, Thomas Sobocinski would attend. Weede confirmed. The ASAC touched base once again on Tuesday morning.

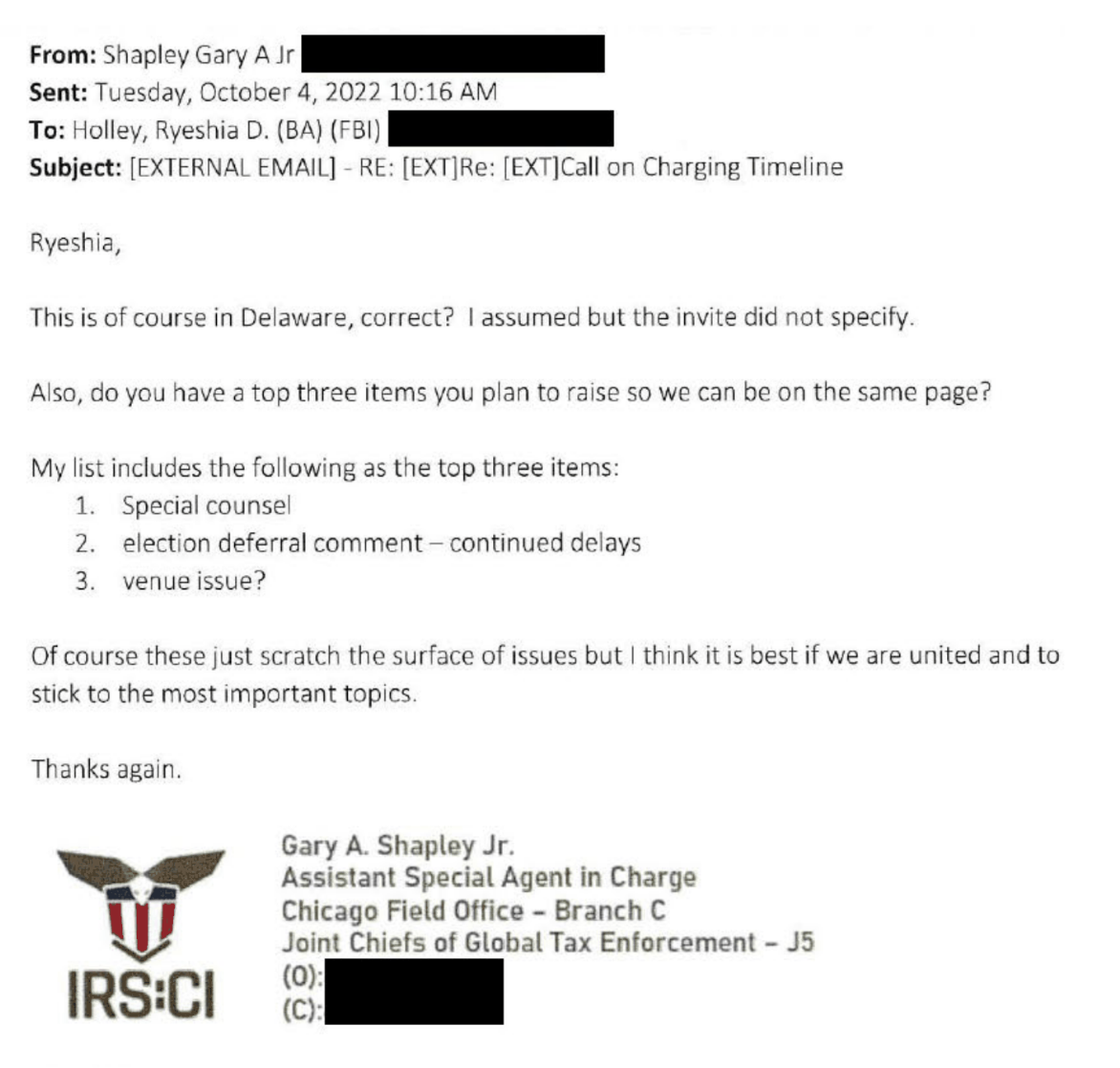

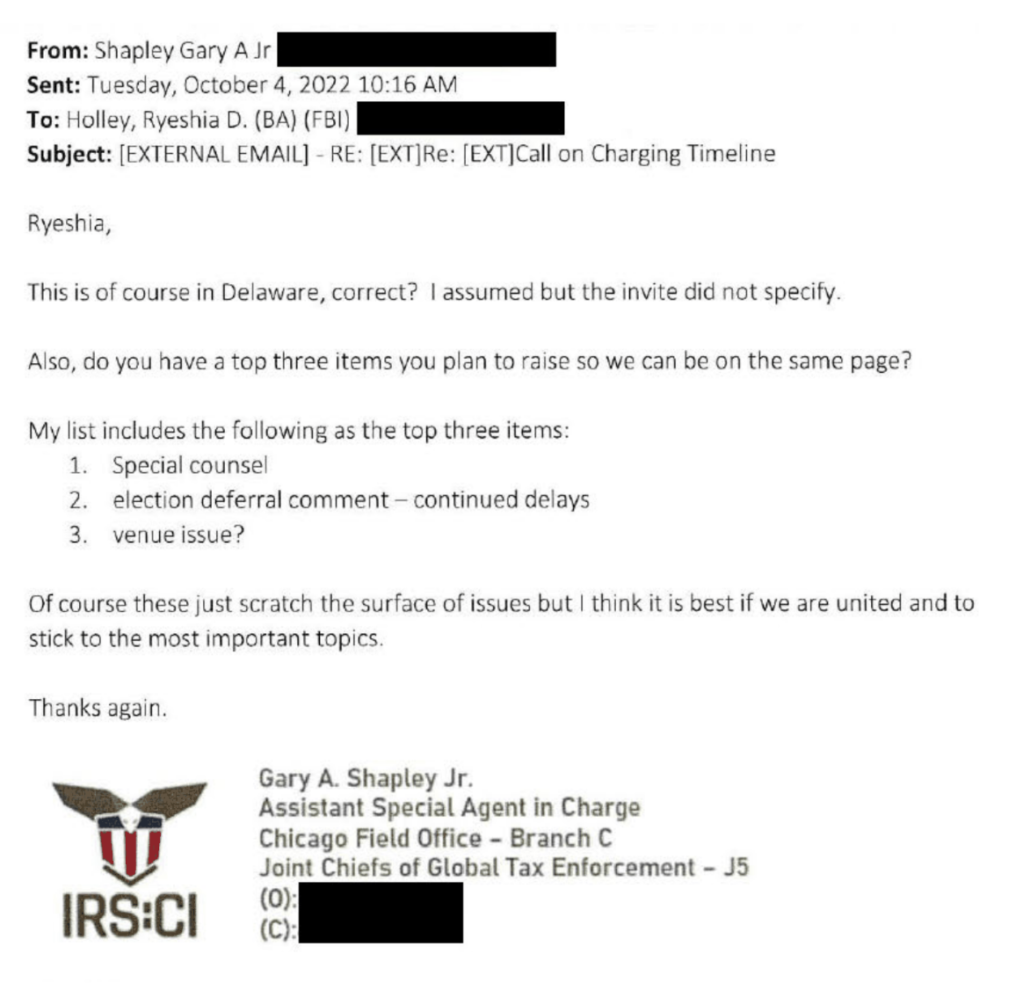

Only at that point, on October 4 — with no record in the thread that Shapley had told his own boss, Waldon, that this meeting was in the works, did he respond to the ASAC alone, asking for her top three items “so we can be on the same page.”

His own list might was effectively a first draft of the things he would record as having happened in notes and a memorialization email days later: Special Counsel, the delay until after the election, and venue.

At 2:26PM, WaPo posted the story that preempted prosecutors’ decision to wait until after the election before charging — the decision Shapley first learned of in July but staged a tantrum about more recently.

At 4:34, the ASAC responded, asking if Shapley’s ASAC (Waldon) would attend, and describing her own agenda as:

- Delays

- Venue

- Communication

- Anything further that develops by tomorrow

Of course: that “anything further that develops” had already developed: the story in the WaPo.

Shapley responded a minute later, saying, he had just tried to call her, but that yes, both Shapley and his SAC would attend.

Nine minutes after that exchange occurred with no mention of the WaPo story, Shapley informed his bosses about it.

Just an FYI that there was a media leak today purportedly from the “agent” level on Sportsman. I imagine it will be a topic of discussion at tomorrows meeting in Delaware. I spoke with Justin Cole about this to provide anything he may need.

I have no additional insight that is anything but a rumor.

Federal agents see chargeable tax, gun-purchase case against Hunter Biden – Espotting.com

Just keeping you informed.

[Link to original WaPo story, but note that Shapley shared an Espotting link]

As I’ve noted, Shapley’s reference to rumors is inconsistent with his past statements about the leak.

As all that was going on, the other DE AUSA besides Wolf, Carly Hudson, wrote Ziegler at 10:07AM on October 6, asking him what he was supposed to remind her about — something he heard immediately after the James Biden interview on September 29.

David asked me to remind him what you [s]aid “regarding the call you received from management after the James Biden meeting.” I’m not 100% sure what he means. Would you mind reminding me about that call so I can remind him?

Ziegler didn’t respond until 6:51PM, well after the WaPo had published the story. Ziegler explained that IRS management had been informed that DOJ Tax didn’t anticipate charging until 2023; they weren’t done with the approval process.

They heard from DOJ-Tax that they don’t expect the case to be indicted until 2023 as they still have various levels of approval. I think this is what you are asking about.

There’s no documentary record of it, but it would be inconceivable that Ziegler hadn’t shared this with Shapley when he heard it, on September 29. Which is to say that Shapley knew there were reasons — beyond the fact that James Biden wasn’t interviewed until September 29 and beyond the election — why Hunter wasn’t going to be charged until after the election.

Nevertheless, going into a meeting he would much later pitch as his “red line,” a meeting that ended up significantly focused on a pre-election leak promising charges, Shapley would claim the election was what was causing the delay.