The Slow Death of Neoliberalism: Part 3 The Phillips Curve and Critical Theory

I described attacks on the Phillips Curve in Part 2. This part discusses the history of the Phillips Curve in detail, and concludes with a discussion of the problems revealed by the failure. The Observations are the fun part if this is too long.

History of the Phillips Curve

This section is based on parts 1-3 of The History of the Phillips Curve: Consensus and Bifurcation by Robert Gordon, an economist at Northwestern, published in the 2008 in the journal Economica at p. 10 et seq. (behind paywall, but available online through your local library). In 1958, William Phillips published a paper which as Gordon puts it,

… replaced discontinuous and qualitative descriptions by a quantitative hypothesis based on an unusually long history of evidence. Since 1861 there had been a regular negative relationship in Britain between the unemployment rate and the growth rate of the nominal wage rate. P. 12.

Phillips fitted a curve to data from the period 1861-1913, and plotted data for the remaining periods, through 1957 against that curve to find disagreements. Phillips found that his curve was close across the entire time except for a couple of years that he explains away. Here’s the curve Phillips fitted to his data:

1) wt = -.90 + 9.64U-1.39

Gordon says “… the inflation rate would be expected to equal the growth rate of wages minus the long-term growth rate of productivity.” P. 12.

1a) p = w – k

For some reason p is inflation and k is productivity. Upper case letters are levels and lower case letters are rates of change. So equation 1 can be written

2) p = -.90 + 9.64U-1.39 – k.

Paul Samuelson and Robert Solow discussed the Phillips results in the US context in a 1960 article. They found no similar data for the US, but they did some estimates and suggested that the PC doesn’t fit their data for several periods, and that it can shift up and down. Phillips estimated that an unemployment rate of about 2.5% was consistent with zero-inflation, while Samuelson and Solow think it might have been 3% pre-World War II and was about 5-6% in the early 60s.

With this seal of approval, the idea was incorporated into econometric models in two equations. In one, the PC was embodied and other variables were added, including demand, unemployment, the rate of change of unemployment, taxes, expected inflation and others in different combinations. This result was fed into an equation that calculates inflation based on wage levels, price levels and trend productivity. Gordon explains that

The reduced form of this approach implied that the inflation rate depended on the level and rate of change of unemployment, perhaps other measures of demand, and lagged inflation.

This is followed by a long discussion of the views of the Chicago School, which Gordon dismisses as utter failures. Moving along to 1975, Gordon turns to efforts to modify the Phillips Curve by adding supply and demand shocks. The price of oil shot up in 1973 because of OPEC. The demand for oil doesn’t decrease quickly in the short run, so people spend more on oil and less on other things. The Phillips Curve didn’t predict the results. Gordon says

The required condition for continued full employment is the opening of a gap between the growth rate of nominal GDP and the growth rate of the nominal wage to make room for the increased nominal spending on oil. P. 21, cite omitted.

That means wages must fall, Gordon says, or we have to add money to the economy, but the latter would lead to inflation. What we actually did, he says, was wage rigidity, increased unemployment, and some nominal (meaning not adjusted for inflation) GDP growth. Gordon then developed and published this version of the Phillips Curve:

3. pt = Ept + b(Ut – UtN) + zt + et

The second U term is the “natural” rate of unemployment, which I’m not going to take up. The z term represents cost-push pressure from unions and supply monopolies. The e term is apparently a constant but it seems odd that it might vary over time. Gordon explains that this version incorporates inertia, the idea that if there’s inflation in one period, there will be inflation in the next. It also reflects supply and demand issues, like wage and price rigidity.

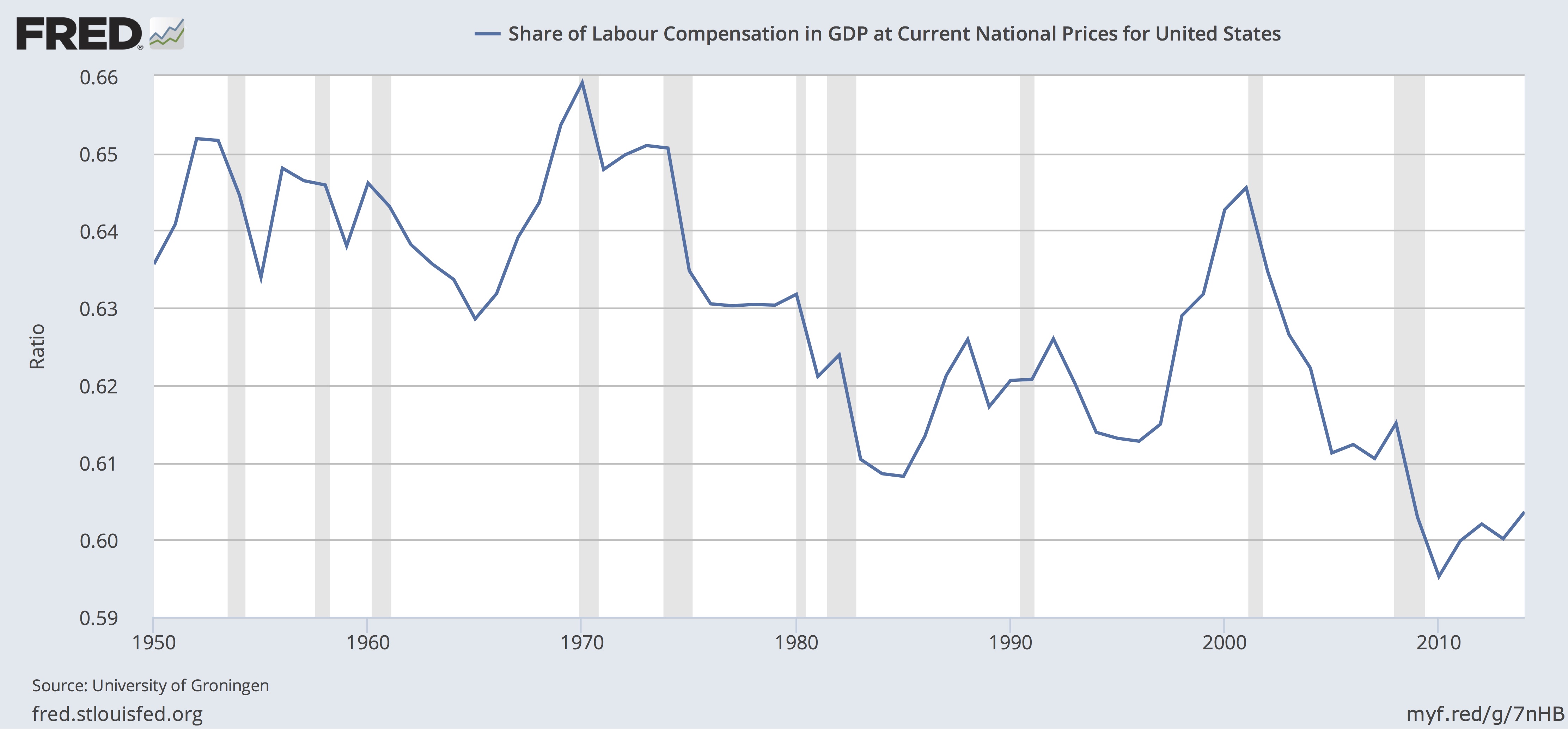

Gordon then mentions in passing that the wage equation (Equation 1a) is only valid if labor’s share of the GDP is fixed, but it isn’t. Here’s a chart from FRED

That problem, says Gordon, is “fruitfully ignored”. We don’t need to consider wages, we just look at prices. With these changes, we can understand the past by explaining away variations with negative or “beneficial supply shocks” and other variables. Gordon says that Equation 3 is foundation of the mainstream model. There is a related model, the New Keynesian Phillips Curve which is similar except that it incorporates future expectations of inflation, and makes no specific provision for supply and demand shocks. I assume these in some combination are the models used by the Fed, and heavily criticized as discussed in Part 2.

Observations

The concept is replaced by the formula, the cause by rules and

probability. Dialectic of Enlightenment, Horkheimer and Adorno,p. 3.

1. Phillips was working off empirical data when he fitted his curve, data about inflation and the rate of growth of wages. There are some theoretical issues in the preparation of that data. But the only abstract theory he adds to his data is Equation 1a, which Gordon says has a solid base in intuition. At the time he was writing, Phillips would only have seen data supporting that theory. We have new information:

As it happens, and perhaps not surprisingly, Phillips’ Equation 1 doesn’t work on US data. Gordon himself and others start adding things to make the Philips Curve work. They are convinced that there is a link between unemployment and inflation, and that they just need to add the relevant variables from their theoretical arsenal to get it to come out. Some focus on expectations, others on supply and demand shocks, and others add taxes or something else. Once they get those pesky variables set up, it’s just a matter of solving for constants. The point is to fit a curve to the actual data, not to use the actual data to see what’s happening. The concept connected to the real world is gone, replaced by the formula. The cause is replaced by the rules of economics.

2. If we set inflation at 0 in Equation 1a, the rate of wage growth is equal to the rate of productivity growth. As the above chart shows, this relationship broke about 50 years ago. If all the gains from productivity are not going to labor, they are going to capital. Of course, capital takes several forms, for example, housing, agricultural land and other domestic capital. See, Piketty, Capital in the Twenty-First Century, Figure 4.6. When you think about it, it seems almost impossible that some of the gains from productivity weren’t going to capital all along. But in the current economy, it’s obvious that companies like Facebook can provide vastly more services with disproportionally fewer additional employees, few of whom are well paid, so that most of the gains from increased sales go to capital. Or, suppose that manufacturing is outsourced, reducing labor costs. Some of the gains might go to cutting prices but surely some go to capital. Let’s rewrite Equation 1a to reflect this, using γ for the growth rate capital.

1b) p = w + γ – k.

Using Equation 1b instead of 1a, we would have this instead of Equation 2:

4) p = -.90 + 9.64U-1.39 + γ – k.

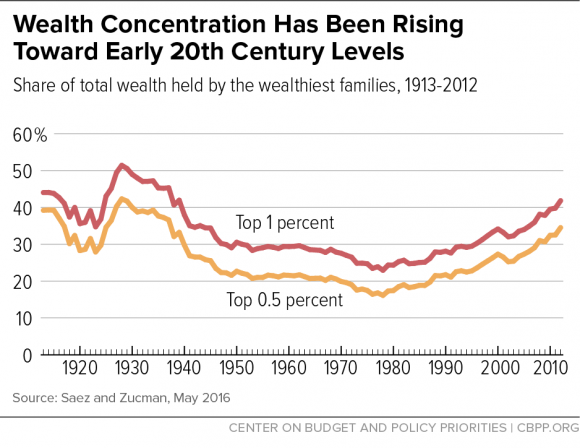

This equation focuses attention on the changes in the return to capital. That issue never seems to trouble most economists, but the rate of return to capital is the central focus of Piketty’s Capital In The Twenty-First Century. This chart from the Center on Budget and Political Priorities shows that top wealth started on its climb at the same time wages diverged from productivity, which supports the idea that gains from productivity are going to capital:

It also calls attention to the fact that nowhere in Gordon’s paper is there a mention of power, market power, political power, or social power, all of which Piketty talks about. Actually, hidden away in Gordon’s article is a backhanded reference to power. Equation 3 (Equation 7 in Gordon’s paper) includes a term “…zt to represent ‘cost-push pressure by unions, oil sheiks, or bauxite barons’”. P. 22. Obviously Gordon understands that the power to control the price of goods and services could create a negative supply shock, and the loss of control could produce a beneficial supply shock. P. 25. However, this is not explicit, and it certainly doesn’t deal with our current economy, in which almost all goods and services are dominated by a small number of gigantic companies exercising a significant degree of price control.

The tweaking Gordon describes might work for a while, but as the degree of price control through monopoly and oligopoly power increases, and γ becomes a bigger factor, the tweaks quit working.

3. Let’s put this in a larger context. For many economists, the Phillips Curve is structural. But why would you think so? It seems more likely that the relationship holds in a certain set of social conditions, including legislation and regulation, power conditions, and people’s attitudes. A logical use of the data is to work out the conditions that must exist to make it so. That’s how Piketty approaches his inequality data.

It’s a mistake to use a coincidence to predict the future. It seems to be a particular problem in economics. Even people who seem to know better continue to believe in the Phillips Curve. Here’s the President of the Boston Fed, Eric Rosengren:

A number of papers at the conference highlighted that some of the economic relationships that are frequently assumed to be stable over time have proven to be not so stable as we have come out of the financial crisis. These structural changes mean that if you tried to have a model that was fairly invariant to these changes, or a process that was invariant to these changes, there would start being big misses in monetary policy.

He goes on to explain that we have to raise interest rates because maybe not the Phillips Curve, but when employment goes up, inflation goes up. Rosengren knows there’s a problem, but he doesn’t have any idea of how to cope, so he keeps doing what he thinks he knows is right. It’s another example of Horkheimer and Adorno’s statement in action.

Updated to define γ more exactly.

Have you seen Piketty’s paper on Putin and the oligarchs?

https://gabriel-zucman.eu/files/NPZ2017.pdf

Continuing to do “what you know is right”, despite it not being right, and expecting it to be right in the future. Is that a variation on the definition of insanity?

Surely, the Phillips curve is an attempt to analyze historical data, to look for patterns, if found, to assess whether or not they hold up under changes in circumstances, and how sensitive such patterns are to changes in those circumstances. At what level of change do the patterns fail and change the “curve” into another shape altogether.

It would seem to be poor methodology to conclude that patterns exists and then to shoehorn exceptions into variables or “constants” in order to preserve those patterns. When do the exceptions swallow the rule?

If the PC is an attempt to create an economic “law”, it should apply across national economies and over vastly different circumstances: different states, forms of government, size and make-up of economy, regulatory, social, legal, economic and business climates, degrees of and trends in market concentration, war, depression, and so on. At some point, changes in variables should make the pattern fail.

One would think that economists’ lack of interest in history – especially their own – would suggest that it is premature to use the PC as a predictor of anything but departmental research budgets. Using it as a guide to government or business policy would seem to be pushing a rope.

Regarding share of labor compensation in GDP. There does not seem to be any accounting for the shift in FICA taxes from twice 5.85 in 1977 to twice 7.65 in 1990. That would derate the typical workers income gain from 109 percent to 102 percent. Another Fed trick is to place hedge funds in the household category where their share of borrowing and income distorts the statistic. Anything to distract from the gains of the 0.001 percent.

I just read through parts 1-3. I agree that the dominant form of economic theory and government policy is certainly neo-liberal, meaning that Capital and Markets are are to be trusted as independent and self-regulating phenomenon that act to create the highest form of social economy (society) as as long as government regulation, public welfare, and organized labor do not interfere. This is certainly only a point of view, but one that is taught with such complete obedience in our educational institutions that it rivals religious fundamentalism in its claim to absolute truth.

The Great Depression galvanized a generation economic thinkers and theorists who felt it was their job to understand how the greatest historical period of human productivity in the 1920’s ended in the worst poverty and unemployment that the country had ever known. The prevailing economic voices did something amazing- they found ways to synthesize and hybridize unrestrained Capitalism (aka neo-liberalism) with Socialism!** Democratic Socialism was FDR and the New Deal. It was the prevailing political economy in Western Europe after WWII. It was what Third World nations in Africa, Asia, and South America tried to adopt in the 50’s – 70’s only to be squashed by our own CIA.

Friedman, Hayek, Ayn Rand, and other “Libertarians” were promoted by the post war big business and the financial establishment to act as an antidote to the prevailing winds of Social Democracy.

Is economics Science? – in the sense that theory can be proven by empirical evidence and repeatable outcomes? No. The math in economics is certainly scientific, but it is only as good as the data examined and the variables considered. That is why the Phillips Curve- while an interesting observation of a couple of economic variables described in a mathematical relationship- is not a scientific law. At the end of the day, it is still just an observation.

I would add that a HUGE variable not considered in the Phillips Curve is interest on money, and private/public debt. You cannot have a discussion about inflation’s effect on wages and unemployment without considering these variables. Contrary to popular economic teaching and Fed policy, raising interest rates increases inflation in the long term. By omitting this variable, though, economists theorize the ridiculous idea of “wage-push” inflation and justify paying labor less! Or, think that high inflation is good for employment! (Or, lowering the tax rate on the wealthy and corporations will raise net income tax collection ??)

My recommendation for an economic treatise worthy of scientific merit (and ironically written by a real Nobel Laureate in Chemistry) is: Wealth, Virtual Wealth, and Debt: The Solution of the Economic Paradox by Frederick Soddy. This guy could run circles around the economic gurus of today.

_______________________________

**not “National Socialism” like 1930’s Germany/Italy… not “Soviet Socialism”…. and socialism is NOT Communism (Communism is State run with no private property and no free markets). Socialism is the part in any political amalgam that considers rights of labor (equitable distribution of income, safe working conditions), and public welfare (education, health care, infrastructure, etc.).

One might also question the political and social judgments behind the PC. “Relationships” between interest rates and employment suggest a preference for one over the other, a political choice, not a mathematical one.

Preservation of capital, via low rates of inflation, benefit the small portion of citizens with large amounts of capital to protect, Rockefeller and Morgan, for example, over the majority of farmers, small business people, and workers living pay day to pay day.

William Jennings Bryan in the 1890s gave voice to criticisms about predatory railroad freight rates and grain elevator prices (market access bottlenecks), tight credit policies and interest rates to farmers that would make a contemporary payday lender swoon. He argued for looser credit policies (silver) that favored farmers, small business owners and workers over tight ones (gold) that favored large capitalists. The latter also lowered borrowing costs to a militarizing government about to rapidly expand its navy and foreign empire, and soon to acquire its canal in Panama. The well-heeled Robber Barons of Bryan’s day helped persuade the USG to chose gold, hence, Bryan’s Cross of Gold speech. Preserving capital rather than preserving employment remains the gold standard for economic policy.

In the case of the British data on which the PC was originally developed, it would have to have been examined, e.g., for peculiar imperial effects. Examples include access to artificially low cost resources from the empire, protected export markets within the empire, sterling’s role as a global currency, limited labor mobility and early stage unionization, an early lead in the technologies of production, and significant changes in government policies. These range, just before and during the period, from changing protection of domestic landowners and ag producers (England then had the most concentrated land ownership in Europe) into subsidization of manufacturers, to the introduction of early social protections for children, the sick, the elderly and the unemployed (a process that precipitated more than one constitutional crisis). And there were the social, political and economic consequences of WWI, a depression that lasted longer than the one in the US, and WWII.

it seems to me in policy debates that economic theory and economic findings are frequently in thrall to a proposed public policy. that means in thrall to those ideologies, institutions and individuals behind a policy proposal, say a tax cutting policy being loudly bruited about :)

whatever merit the economic theory behind the policy may have (which may be little to none), one should always look for the “little tweaks” that betray the policy as some powerful political force’s fav solution, not as a straightforward application of economic theory. a simple example is the failure of the obama administration to add sufficient federal government stimulus to the economy early in the great recession because republican congressional forces (and some debt-oriented dems) “worried” about debt.

in this view economic findings or theory are dragged out into public from time to time as a sort of argument to authority. but that the policy follow the theory

may be of no concern to the policy makers. their concern may be to achieve the policy result that will satisfy their economic needs and those of their followers’ (often rent seeking).

for the current tax reduction argument i would expect to see the ghost of the laffer curve show up frequently in public debate together with other sophistical public relations tricks from the supply-side economics policy quiver.

matt writes:

“… Is economics Science? – in the sense that theory can be proven by empirical evidence and repeatable outcomes? No. …”

it’s a free country, but why would one even want to argue that so well-developed an area of human interest and inquiry as economics is not a science? what’s to be gained? there’s a feel of ideology about such a claim.

as i have noted before, it makes as much sense to claim that mormonism is not a religion as to claim economics is not a science. by virtue of the commonly accepted intellectual and emotional rules their supporters obey, they are religion and science respectively.

“… not proven by empiricle evidence and repeatable outcomes..”

certainly much economic literature is clearly based on empirical evidence. some outcomes (usually of very small scale experiments) are repeatable, or better, testable by popper’s emphasis on falsification rather than “proof”. other areas of economics are very large scale data collections about which economists make educated guesses. those guesses may prove useful. they may be shown to be unreliable, e. g., phillips curve. they may prove wrong or contradictory to related theory.

can anyone who knows economics claim there are no or few useful insights we can use from this vast body of human intellectual activity?

economics is a social science. the social sciences have developed their own criteria for validating studies, criteria in some important ways different from the physical sciences. each has its own collection of philosophers of science and methodologists. that they are different does not mean one is useful and the other useless.

for example, psychology these days is having a grand fight about reproducibility of results, and about time, too. part of this fight involves the misuse or misundestanding of how to use the p-statistic. that misunderstanding extends to the physical sciences as well. economics has been moving away from its a priori beginnings for a hundred years and is now developing the field of behavioral economics which will probably come to form a basis for microeconomics in time.

i prefer karl popper’s view of science as intellectual activity that can be falsified, as opposed to that which must be proved or repeated. falsifiability seperates science from religion – and from ideology :)

“economics is a social science.” That’s much better. That distinguishes economics from actual sciences like math, physics, chemistry and biology. No one has argued that economics cannot be useful, just that there is no assurance it will provide useful guidance, nor does it have the rigor of an actual science. p = w – k cannot be applied like A=pi(rsquared) to determine the area of a circle every time, nor does it always work across cultures. As demonstrated above, economic trusims like the Phillips Curve actively misguide economic policy.

That “social” modifier makes a world of difference. Syphilis is a “social” disease, it comes from people screwing one another, much like neoliberalism.

lefty, always the ideologue, informs us that:

“… That distinguishes economics from actual sciences like math, physics, chemistry and biology. No one has argued that economics cannot be useful, just that there is no assurance it will provide useful guidance, nor does it have the rigor of an actual science…. ”

lefty, the world is not divided into “actual sciences” and the rest, except by ideologues like you. reasonable people seem to agree that there are sciences from anthroplogy to zoology which employ many different ways of collecting and analyzing data; there is no one “rigor of an actual science”.

many sciences provide us with “useful guidance”. that includes economics which has provided us with, for example, insight and guidance (strong gov’t spending during recession) to avoid the trap set by the austrian school – inflation control as the highest priority.

at any one time no science can provide more than modest assurance its guidance is useful. that’s why, for example, we have drug companies test their chemicals and why paradigm shifts, e. g. geology and plate techtonics or the ether and james clerk maxwell, are so important.

You two have had this argument already. Let’s not do it again.

exactly my opinion.

this crap destroys the pleasure of participating.

i made my points at 1:36 in response to a comment matt made. they were important considerations.

“this crap destroys the pleasure of participating.” Indeed it does. Thank you Ed for a very nice series on the death of neoliberalism. Hope there are more parts to come.

I think this three part series was designed to challenge an economic theory- to make the point that math (as in mathematical proof) does not function in the same absolute form for economics as is does for chemistry or physics.

In the current age of Capitalism, the high priests of economics have ignored the emphasis on social questions and ethics that was a key element of the profession before WWII. Laws (as in laws made by the State) and Gov’t policy making for trade, finance, stock market investment, employment, taxation, infrastructure, healthcare, and education are made based on the assumption that prevailing economic theories have evolved from hard scientific facts and mathematical proofs.

I don’t think anyone is saying that Science cannot be applied to economics, or that there is not a vastly useful knowledge base in the economic profession. The issue that so badly needs to be understood in Washington, on Wall St. and in academia is that neo-liberal economic theory has deified Capital and Markets to the point where people and social issues don’t matter anymore.

I would say, that if you are very, very careful you can approach economics with scientific vigor. But, you can also use science to justify your ideological bias, promote the agendas of special interests, or even worse to perpetuate outright fraud.

Are CEO’s, bankers, investment brokers, politicians, and media figures not “ideologues?” Do they not “believe-in” mostly the economic propaganda that spews from business schools and partisan think tanks?

Quoted a Financial Times review of the book mentioned next, “the more one thinks about the function of market economics in modern society, the stronger the case gets for treating it as a religion.” (Economics as Religion: from Samuelson to Chicago and Beyond by Robert Nelson) (Also recommended: A Guide to What’s Wrong with Economics by Edward Fullbrook).

this is a very thoughtful, informative comment, in a word intellectually elegant.

tx.

for myself i always look at the policy and the policy makers and the policy makers’ moneymen for explanation of market dysfunction. in my view economic theory used in the policy realm often serves merely as an argument to authority. go after the policy makers (politicians) and their seducers if you want to change things.

to borrow a phrase from modeling, economic policy is “completely specified”, as is the rest of the american political process at every level. by using this term in this special way i want to point out that all parts of the american political system are now well understood and open to lobbying, “policy bribery”, and rent seeking by those with the most money and the best organization. that means banking regulation, anti-trust/monopoly/oligopoly, loans of all kinds, taxes of all kinds, freeedom from accountability (agreements to arbitrate rather than sue, anti-competitive clauses, bankruptcy law) , defanging of trial lawyers, limitation/destruction of unions – the list is very long in a “completely specified” poltical system where gaming the system is so easy.

…yes, the ideals of any economic paradigm are betrayed by ignorant or intentionally self-serving policy makers. But, in a alternate universe where William Jennings Bryan was elected president and 19th century progressive economics matured in the 20th century, we might be discussing the misconception of an economic equation based on the works of Henry George, Thorstein Veblen, or John Ruskin…

Its not just the failure of policymakers and politicians … its failure of the policy itself, that is, the dominant economic paradigm of neo-liberalism. I might add that this paradigm is quite exclusive, just like a fundamentalist religion that claims one path to salvation. Neo-liberalism does not “mix” with other forms of economic philosophy. In fact, Neo-liberalism has gone one step further to denounce all other economic ideas as heretical, backward, and downright stupid. This happens on all levels from the academics who teach MBA programs to the media personalities we look to for news and commentary.

Rome is burning. Human civilization is in peril. The ends of absolutist Libertarianism is perfect exploitation of all the resources of the Earth, and perfect accumulation of wealth and power to the handful of men and women standing in the shadow of the one true god- Capital. This is Ayn Rand’s fantasy- the immutable success of an immortal Howard Roark.

All the little human actors in this “completely specified” model are programed to run on neo-liberal economic fuel. They have been programed to interpret ANY form of ethical or social concern as Collectivist, Communist, or Socialist, which in most minds equates with the horrors of Stalin & Mao. Oh no! health care, social security, public education, environmental concern! These are the enemies of freedom- slippery slopes that lead to bondage, dictatorship, and the death of America!

I’m a small business owner. I love capitalism and free markets- when moderated with some restraint and consideration for social welfare. But, where we’re headed is exactly where Marx predicted- a second revolution after the endgame of absolute Capitalism.

How to save the world? Encourage regulation of market forces and taxation of excess wealth to balance the system (not so that every body is equal) but that everyone as the opportunity to provide for themselves and their family a decent standard of living. Regulation and taxation, are unfortunately the antithesis of the neo-liberal economic paradigm. Herein lies the problem.

OT, moving on to a non-controversial topic, Mr. Trump’s phone call to a widow of a fallen soldier. It seems to be another example of the way Trump botches things he does only petulantly, because an advisor told him he should do it because it’s what a president would do.

Yes, Trump is incapable of normal human emotions, standard behavior for a malignant narcissist. He believes only his feelings and thoughts of the moment matter: to give attention to anyone else’s is to make an own goal. He politicized the moment as a defense to his own behavior, the way he lies to defend against his earlier lies, then lies again.

Mr. Trump should not be given the benefit of any doubt; he lost the right to that quite some time ago. He should not be judged by his intentions, which are as variable as English weather. He should be judged by what he does. Botching it is what he does. He doesn’t botch it because it’s complicated, he’s busy, or because he’s held to impossible standards no other president has been held to. He blows it because that’s as good as he gets.

Now let’s talk about something less controversial, such as Paul Ryan substituting himself for the president in the hole he dug by refusing to reimburse health care insurers as a way to ensure that faulty but better health care becomes no health care for millions. Ryan throws a rock at a game of marbles because he isn’t winning, because the temporary bipartisan fix doesn’t give him all that he wants, and because a fix doesn’t hurt the little people enough….

And if you’re a father grieving over the friendly fire murder of your soldier son, and the president calls and offers you $25,000 from his personal account because you don’t have two nickels to rub together, don’t spend it before it comes and clears.

By the way, the president might also offer to sell you – at the best price evuh – a very profitable casino, and a hotel, and a couple of high-rise condos. Once they’re out of bankruptcy. Donald Trump: a serial liar, denier, and blame shifter of epic proportions.

Trump & the Alt. Right are a mixed bag when it comes to neo-liberalism. I’m still trying to figure out how protectionism, isolationism, and nationalism (for the benefit of the Working Class?) fits in with trashing healthcare, public education, the environment, civil liberties, and progressive taxation.

As mentioned earlier, in other posts the Clinton-Obama establishment did more for trade/financial deregulation/liberalization than the Bush dynasty. So, I’m not sure we’d be so much better off with Hilary. Bernie rules my political fantasies.

Paul Ryan. What a turd. Bought and controlled by the Koch Bros. He has ruined quite a bit of what was one of the best States in the Union along with my Koch sucking :) Governor Scott Walker.

When it comes to figuring out how protectionism, isolationism, and ultra-nationalism fit in with trashing healthcare, public education, the environment, civil liberties, and progressive taxation, I would argue the two sets have nothing in common and can’t be fit together. That they do I think is rightist propaganda of the sort elites have been selling for generations in order to have one set of have-nots fight another set instead of sharpening their pitchforks for those living in the Newport version of Versailles.

Trashing the public sector is important for several reasons: to deny it legitimacy, to avoid paying taxes, to stop government from doing anything but protect the lives and property of the elite. Public education, for example, takes taxes from the elite and spends it on the masses. Let them eat textbooks.

Ditto re civil liberties: the masses are meant to do as their betters tell them to do, not to decide for themselves nor even to have lives secure enough that they might dream about it. School debt is another privatization of the commons and a tool with which to extort compliance.

The environment doesn’t count unless it contains something the elites want to extract from it. Look at the Congo or what used to be an Appalachian mountain top. The elites must imagine they can drink bottled water while the rest of us scout toxic dumps to look for closed wells. That is, so long as no one with gumption has the wit to ask who is filling their bottles, with what and from where.

Well spoken! What are we to do?

as i’ve noted before, neo-liberal government policy will continue to survive whether neo-liberal economic theory is strong or weak, alive and well or dying. that is because neo-liberal policy benefits the very rich, political moneymen, koch style political organizations, and corporate lobbyists. neo-liberal economics is merely serves as a political fig-leaf for the policies they favor.

https://www.washingtonpost.com/news/wonk/wp/2017/10/20/trump-considers-big-shift-at-federal-reserve-as-he-faces-pressure-to-appoint-republican/?

yellen has done a good job under difficult circumstances; john taylor or kevin warsh are a neo-liberal’s dream.

stay tuned for zombie neo-liberal economic policy.

and rember it’s not only the politicians, the lobbyists, the koch brothers style political organizations, but tens of millions of ignorant/manipulable voters who keep neo-liberal economic policy stalking thru the land.

“but tens of millions of ignorant/manipulable voters who keep neo-liberal economic policy stalking thru the land.” And if they get over Hillary, Bill and elitist, neo lib, DLC “New Dems” and get get back to the New Deal there may be hope for the Party and the country.

OrionATL is the realist, Lefty665 is the idealist. You both are absolutely right.

Close to half the Party is there, just a question of how many more elections the Dems have to lose before the folks with sense get back in the drivers seat. If Hillary keeps up her book tour that will hasten the process. A few of the deluded come to their senses each time she finds someone new to blame for her loss. Schumer and Pelosi showed the way last summer with “A better deal: Better jobs, better wages a better future”.

Hoo hah, “OrionATL is the realist” Oh thank you, I needed a good laugh.

There is room for both of these in coexistence here. But without the bickering like a married couple!

boo! 😅